Accounting delay of WRDS Factors

1 What’s the problem?

It’s common practice to include several, if not dozens, of pricing factors in your empirical model. The computation of these factors is by no means enjoyable. To solve the issue, WRDS launched a product named “Factors by WRDS” or “Backtester” which provides 134 pre-computed pricing factors on a monthly basis.

WRDS offers a comprehensive manual for this product, but there’s one thing it doesn’t address: How do they deal with accounting delay?

To illustrate the problem, consider the factor “Book-to-Market ratio (BtM).” To get the book value, we need to refer to 10-Q/K. Assume that the fiscal year end for a company is Dec 31, 2000, and the 10-K is available on Feb 28, 2001 (the next year). Since there’s a delay between the fiscal year end and the release of 10-Q/K, on Dec 31, 2000, the market wouldn’t yet know the book value of Q4. To compute Book-to-Market ratio, we have to use the value of Q3.

In finance/accounting papers, researchers typically apply a uniform delay to the accounting data. For example, in Sloan’s famous accrual paper (Sloan, 1996), he used a four‑month delay.

The problem is, WRDS doesn’t tell users how much delay (if any) they applied to the computation of factors. So I asked them.

2 Answer: Two months

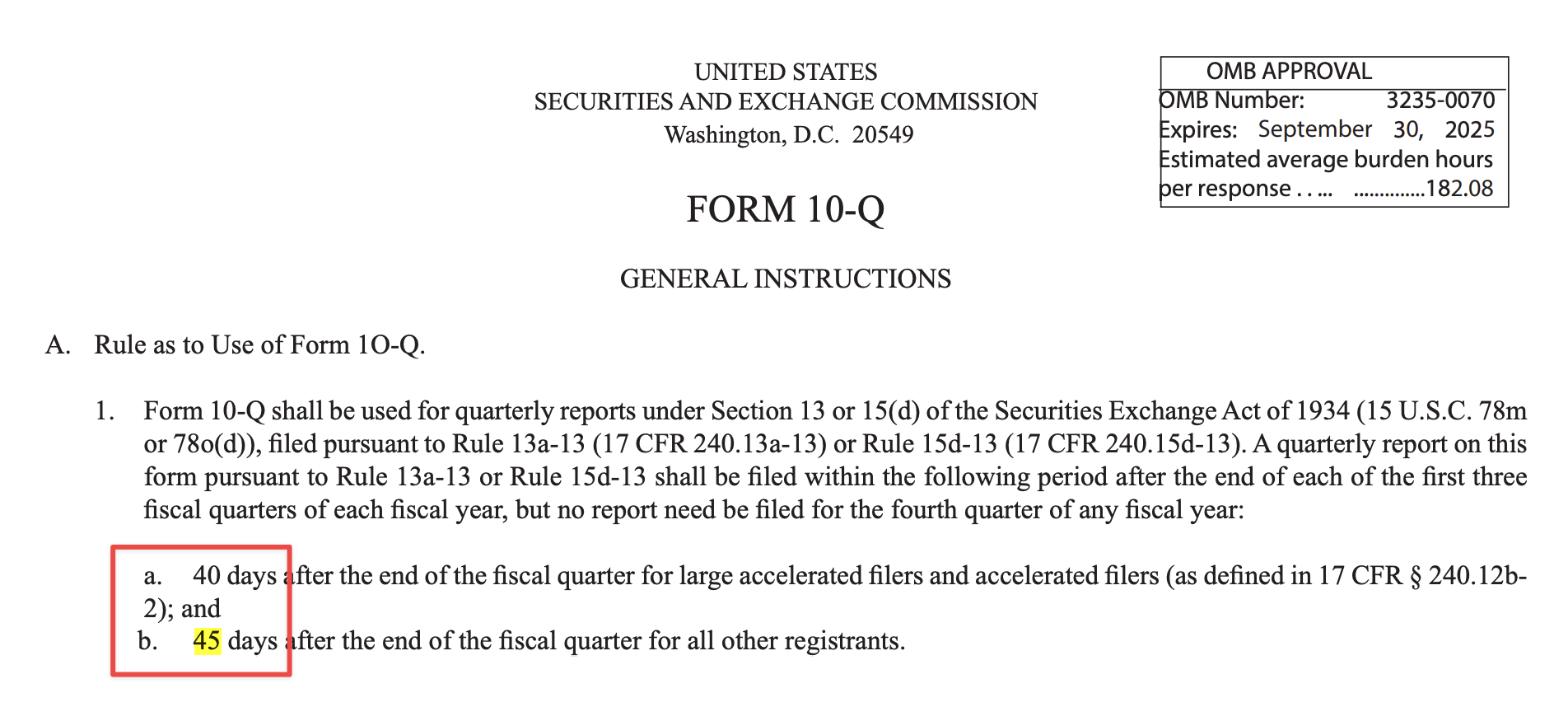

The reply from WRDS is prompt. The answer is two months. That is, at 2000Q4, they’ll only use 10-K/Q of 2000Q3. The two‑month lag is reasonable to me, because the SEC requires public firms to report their 10-K/Q within 45 days.

Reference

- Sloan, R. G. (1996). Do stock prices fully reflect information in accruals and cash flows about future earnings? Accounting Review, 289–315.